How the Chain Began to Rot: 2008 Crisis, Part 2

Part 2 of my series working through the 2008 financial crisis from a real estate perspective. In Part 1, I looked at why the mortgage was trusted for so long. Here I want to trace how mortgage securitization worked in the years leading up to the crisis, and what it did to the incentives of everyone who touches a mortgage along the way.

In Part 1, we left off at what turned out to be the pivot point. The securitization machine that had been built for safe, government-backed loans was about to be pointed at borrowers who carried no guarantee at all. To see why that was so dangerous, it helps to look closely at what mortgage securitization does to the people who make the loans. Because the real damage of the 2008 financial crisis was not financial engineering for its own sake. It was what that engineering did to incentives, all the way down the chain.

Let me walk you through that chain, one link at a time.

The Link That Used to Hold: Skin in the Game

Start with the traditional mortgage from Part 1. A local bank lends a family money to buy a house, then holds that loan for thirty years. What makes that arrangement work is how self-policing it is. The bank that makes the loan is the same institution that eats the loss if the loan goes bad. So the lender has every reason to check whether the borrower can actually repay, because the lender is the one left holding the outcome.

This is the “skin in the game” idea. The party making the decision bears the consequences of that decision. For most of the history of mortgage lending, that alignment was simply built into the structure. Careless lenders went out of business. Careful ones survived. The system policed itself.

It is worth noting that modern CRE lenders still talk about their work in exactly these terms. In healthy debt markets, lenders tend to focus on protecting the downside rather than chasing the upside, precisely because they carry the risk. That is the version of the world that “originate to distribute” was about to replace.

Securitization removed that link almost as a side effect. And once it was gone, everything else followed.

Originate to Distribute: The Mortgage Securitization Model That Changed Everything

The new model, the one that came to define the 2000s, works differently. A lender makes a loan and immediately sells it. The buyer is an investment bank, which gathers thousands of these loans, packages them into mortgage bonds, and sells them on to investors around the world. The original lender gets its money back almost immediately, plus a fee, and then goes out and makes another loan.

This is the “originate to distribute” model, and even at a glance you can see how it rearranges the incentives. The lender no longer earns money by being repaid over thirty years. The lender earns money by originating volume: make as many loans as possible, sell them as fast as possible, move on. Whether those loans are ever repaid becomes, from the originator’s point of view, someone else’s problem.

Michael Lewis describes the moment the industry absorbed this lesson. After an earlier generation of subprime lenders was wiped out in the late 1990s by the slice of loans they had kept on their books, the market could have concluded something simple: that you should not lend to people who cannot repay. Instead, as Lewis puts it in The Big Short, it learned a more complicated lesson: you can keep on making these loans, just do not keep them on your books.

To me, that is the hinge of the whole story. The problem was never that lending to riskier borrowers is impossible. It was that securitization gave the people making the loans a way to make them without owning the risk.

Follow the Payment, and You Find the Flaw

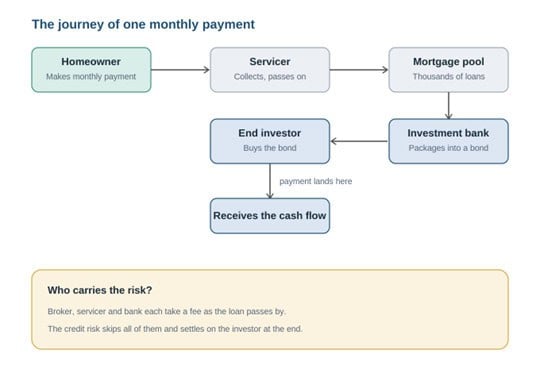

Let me make this concrete, because the mechanics are simpler than the jargon suggests. Follow a single monthly payment through the system, and at each stop notice who gets paid and who carries the risk.

A homeowner sends in a mortgage payment, say $2,000 for the month. Before that payment ever moves, a mortgage broker has already found this borrower and closed the loan, earning a commission for doing so. Notice what the broker was paid for: closing the loan, not making sure it gets repaid. The incentive was volume.

The loan itself was made by an originating lender, but it did not stay there. Within weeks the lender sold it, booked its fee, and used the cash to make another loan. That lender was also paid for volume, and carried almost none of the long-term risk.

So when the $2,000 arrives, it does not go to whoever made the loan. It goes first to a servicer, a company that collects payments and passes them along, keeping a small administrative fee. From there it flows into the pool, the bundle of thousands of mortgages I described in Part 1. The investment bank has already carved that pool into a bond and sold it, earning fees on assembling and distributing it. Its incentive is throughput: keep the pipeline full.

Finally the payment flows out to the end investor who owns the bond, maybe a pension fund in Norway or an insurance company in Japan. This is the only party in the entire chain whose money is actually at risk if the homeowner stops paying. And it is the one party that never met the borrower, never saw the loan file, and trusted instead the rating agencies and the belief from Part 1 that home prices do not fall nationwide.

That is the whole journey, from a homeowner’s checking account to a global investor, in a handful of automated steps. The payment flows cleanly from homeowner to investor. A fee stays behind at every stop. The credit risk sails past all of them and lands on the party at the end who had the least to do with the original decision.

What stands out to me is what that arrangement does. At no point in the chain does anyone whose money is truly at risk actually meet the borrower. The people who assess the borrower keep no stake. The party that keeps the stake never assesses the borrower. Cash flows down, fees leak out along the way, and risk collects at the bottom. The link between decision and consequence, the thing that made mortgage lending safe for decades, is cut into pieces and spread so widely that nobody along the chain feels it.

Hold on to that picture going into Part 3, because that is where the investment bank takes this single stream of payments and slices it into layers. The real engineering starts there.

The Accounting Trick That Hid the Rot

There is a further twist that made the model even more seductive. Even on the small slice of loans originators did keep, they were allowed to book the expected future value of those loans as profit today. The accounting rules let them assume the loans would be repaid, and repaid on schedule.

As Lewis recounts, that single assumption became the engine of their eventual collapse. A lender could report glowing earnings built entirely on the premise that its loans were good, while disclosing almost nothing about how many borrowers were already falling behind. The profits were real on paper. The losses were real in the world. For a while, only the paper was visible.

The Scale of Mortgage Securitization Before the 2008 Crisis

If securitization had stayed a marginal practice, none of this would have mattered much. It did not stay marginal, and the scale is what makes the story land. The figures that follow come from Michael Lewis’s account in The Big Short (Chapter 1, “A Secret Origin Story”).

In the mid-1990s, a big year for subprime lending was around $30 billion. By 2000, subprime lending had reached $130 billion, and roughly $55 billion of that was repackaged into mortgage bonds. By 2005, there were $625 billion in subprime mortgage loans, and $507 billion of that found its way into mortgage bonds. More than half a trillion dollars of subprime mortgages turned into securities in a single year.

The mix of loans was shifting too, in a direction that made them more dangerous. In 1996, about 65 percent of subprime loans were fixed-rate, so at least a borrower knew what was owed each month. By 2005, roughly 75 percent were some form of floating-rate, typically fixed for just the first two years before resetting higher. The product was being engineered, whether by design or by drift, to put borrowers on a clock, a point I will come back to in Part 5.

The most telling detail is that subprime lending was booming even as interest rates were rising, which on its own makes little sense. When the people making loans no longer bear the risk, volume stops responding to risk. It only responds to fees. And the fees never stopped.

Where the 2008 Crisis Story Goes Next

By the mid-2000s, the shape of American mortgage lending looked very different from where it started. The loan was no longer really a relationship between a bank and a borrower. It was raw material, fed into a machine that manufactured bonds, with everyone along the line paid to keep the machine running fast rather than running safely.

But there is still a piece missing from the picture. Turning a pile of risky subprime loans into bonds that conservative investors worldwide would actually buy took more than just packaging. Those loans had to be sliced, layered, and re-rated until the riskiest mortgages in America could somehow carry the same AAA stamp as U.S. Treasury debt.

That layer of the story, the world of tranches, CDOs, and the rating agencies that blessed them, is where we go in Part 3. It is the step that turned a lending problem into a global one.

For now, hold on to the core idea: securitization did not just move mortgages around. It broke the link between the people making lending decisions and the people bearing the consequences. Once no one in the chain had skin in the game, the only thing left to optimize was volume, and volume is exactly what the system delivered.

Sources and Further Reading

This series draws on two works that, read together, tell the human story of the 2008 crisis. Anyone who wants the full account should go to the originals:

Lewis, Michael. The Big Short: Inside the Doomsday Machine. W. W. Norton, 2010.

Sorkin, Andrew Ross. Too Big to Fail. Viking, 2009.

Frequently Asked Questions about Mortgage Securitization and the 2008 Financial Crisis

What is the "originate to distribute" model?

The originate to distribute model is a lending approach where a lender makes a loan and immediately sells it rather than holding it. The lender earns money through origination fees and volume rather than through repayment over time. This model fundamentally changed the incentive structure of mortgage lending: once lenders could sell the loans they made, whether those loans were ever repaid became someone else’s problem.

What does "skin in the game" mean in lending?

Skin in the game means that the party making a financial decision also bears the consequences of that decision. In traditional mortgage lending, the bank that made the loan held it, so a bad loan directly hurt the lender. That alignment created a built-in incentive for careful underwriting. Securitization removed that alignment by allowing lenders to sell their loans almost immediately, spreading the risk to investors who had no role in the original lending decision.

Who are the parties in the mortgage securitization chain?

The chain runs from the mortgage broker (who finds the borrower and earns a closing commission) to the originating lender (who makes the loan and sells it quickly) to the servicer (who collects monthly payments for a fee) to the investment bank (which pools and packages the loans into bonds) to the end investor (a pension fund, insurance company, or similar institution that actually owns the risk). Each party in the chain earns fees. Only the last party bears the credit risk.

Why did subprime lending grow so fast before the 2008 crisis?

Subprime lending grew because the originate to distribute model decoupled loan volume from loan quality. Lenders were paid for closing loans, not for the performance of those loans over time. With that incentive in place, lending expanded regardless of rising interest rates or deteriorating borrower quality. Subprime originations grew from roughly $30 billion in the mid-1990s to $625 billion by 2005, with over $500 billion packaged into mortgage bonds in that year alone.

What is a mortgage servicer?

A mortgage servicer is a company that collects monthly payments from borrowers and passes them through to bondholders, keeping a small administrative fee. Servicers do not own the loans and typically do not bear credit risk. Their role in the crisis was largely structural: they were one more link in a chain designed to move money efficiently, with no party along the way responsible for whether the underlying borrowers could actually repay.

How did accounting rules make the crisis worse?

Originators were permitted to book the expected future value of loans as profit at the time of origination, assuming the loans would be repaid on schedule. This allowed lenders to report strong earnings while the actual performance of their loan portfolios was quietly deteriorating. Profits appeared real on paper while losses were accumulating in the real world, and for a significant period the paper version was all that investors and regulators could see.

What were adjustable-rate mortgages and why did they matter?

Adjustable-rate mortgages (ARMs) carried an interest rate that was fixed for a short initial period, typically two years, before resetting higher. By 2005, roughly 75 percent of subprime loans were some form of adjustable-rate, compared to about 35 percent in 1996. These products effectively put borrowers on a clock: payments were manageable at first, but the reset would force a reckoning. When home prices stopped rising and refinancing was no longer an option, millions of borrowers hit that reset with no way out.

What comes next in this series?

Part 3 covers the financial alchemy that turned pools of risky subprime loans into bonds that conservative investors worldwide were willing to buy. That process involved slicing loan pools into tranches, creating instruments called CDOs, and relying on rating agencies to stamp much of it AAA. It is the step that transformed a lending problem into a global financial crisis.